Best Way to Owner Finance a House in Nc

Go our 43-Page Guide to Real Estate Investing Today!

Real estate has long been the become-to investment for those looking to build long-term wealth for generations. Permit us help you navigate this asset form past signing upwards for our comprehensive real estate investing guide.

In most real estate transactions, properties are bought or sold with bank financing or cash. If the buyer doesn't have enough money to purchase it outright, he or she will undergo intense banking company underwriting to qualify for a loan.

Most people don't know that there'south another way to buy and sell homes: owner financing. Permit's explore what owner financing is, how it works, why a buyer or seller would want to apply it, and important things to know nearly it.

What is owner financing and how does it work?

Owner financing, also referred to as seller financing, is a method of financing a property in which the owner of the property holds the buyer'due south loan. Possessor financing can likewise be chosen seller financing, seller carryback financing or seller carryback (because the owner "carries back," or holds, the financing). It works like depository financial institution financing, just the buyer repays the seller by making monthly payments over an agreed-upon flow with a specified interest charge per unit and terms. Seller financing is commonly used by investors to buy or sell backdrop, but it tin can exist used by anyone.

While this way of financing properties is less mutual than traditional methods, it's a viable selection and more common than you might think. According to Avant-garde Seller Data Services, $25.9 billion of possessor-financed loans were created in 2022 throughout the Us.

There are no restrictions on who can use possessor financing or what blazon of holding tin can be bought or sold with it. I take feel with offering owner-financing deals and buying with possessor financing on a fourplex, a single-family home, an flat circuitous, and a cocky-storage facility. Seller financing is used frequently past real estate investors, but can also be used if a buyer doesn't qualify for traditional financing considering of employment, previous bankruptcy or foreclosure, or economic factors that tighten lending guidelines.

Available Seller Financing Structures

In that location are several types of seller financing structures available:

- Note and mortgage.

- Country contract, which can also be called a contract for act or agreement for act.

- Lease option.

A note and mortgage is the nearly secure class of financing and is the same structure banks use when lending on a property. The seller creates a note outlining the amount borrowed and terms for repayment. The mortgage securitizes the seller with the holding in the event of default. The buyer is put on the title with a deed and the mortgage is typically recorded in public records.

A land contract can also be called a contract for deed or agreement for human activity and works similarly to a note and mortgage. However, instead of the heir-apparent gaining championship to the property, the seller remains on championship until the debt is repaid in total.

Some sellers prefer the structure of a contract for human activity considering it can exist faster and more than cost-constructive to regain title in the event of default. Many states allow eviction or forfeiture, which are faster and cheaper than a total foreclosure. The procedures in the event of non-payment vary from state to state.

A charter option is a slightly unlike structure -- information technology starts with the heir-apparent leasing the home for a menstruum of time with the option to purchase. The buyer and seller concur on the purchase cost of the home before the lease starts. When it expires, the buyer can purchase the home or forfeit their lease option and any fees paid to enter into the charter option agreement. If the buyer buys the dwelling house, payments fabricated during that lease menstruation tin be used toward the purchase of the home.

Repayment terms vary, and in nearly circumstances, they're adamant past the seller but tin exist negotiated by the heir-apparent. Information technology's not uncommon for interest rates to be higher than a traditional bank loan. The seller carries some risk by lending to someone who may non qualify for a bank loan.

Possessor financing instance

Allow's say a seller lists a property for $200,000. A potential buyer cannot qualify for traditional financing because he's cocky-employed. He makes a total-toll offering and requests owner financing with 15% ($thirty,000) down.

The seller has no mortgage on the property and decides to take the offer, creating a mortgage note that requires the buyer to pay her back over ten years at eight% involvement with a balloon payment at the cease. The buyer makes a monthly payment of $one,247.40 to the seller and the seller makes an 8% return, collecting $224,532 over the entire 10-year period.

| Loan Factor | Value |

|---|---|

| Buy price | $200,000.00 |

| Down payment | $30,000.00 |

| Loan amount | $170,000.00 |

| Involvement rate | viii% |

| Number of payments | 180 |

| Balloon payment due at the end of yr 10 | $130,528.65 |

| Monthly payment | $1,247.forty |

| Total paid to seller | $224,532.00 |

Data source: Author calculations.

While this is one case of owner financing, many variables can change how a seller finances a property.

Owner financing terms

It'due south up to the buyer and seller to determine the terms of the deal, such every bit the length of the loan, the amount of the down payment, the interest rate, and if at that place's a balloon payment. Some sellers have specific terms in mind, while others are open to negotiating. However, you need to make up one's mind on iv main factors.

Length of the loan

This is the period over which the buyer will repay the loan. It can exist five, x, xv, xx, or thirty years -- or anything in between. While thirty-yr mortgages are sometimes used in seller financing, it'due south more common to see shorter terms, such every bit five to 10 years, with a balloon payment at the finish. Fifty-fifty if a balloon payment is agreed upon in yr 10, the loan can be amortized for xxx years to proceed the heir-apparent's monthly payment low and increase the interest collected past the seller.

Downwardly payment

A downwardly payment is the amount of money the buyer pays to the seller to evidence their investment and interest in the home. This coin is applied toward the buy price and the residue of that price is financed. The boilerplate down payment for residential properties on seller-financed loans in 2022 was 19%.

While there are ways to buy or sell a property with zero or very piddling money down, this is rare. In most circumstances, sellers require x% to xx% downward, although there's no minimum requirement. A study conducted in 2022 by Black Knight and the U.S. Department of Urban Housing and Development plant that college downwards payments reduced delinquency and default risk. A college down payment shows that the buyer has "pare in the game," meaning they're less likely to walk away or stop paying.

It's of import to note that a loftier down payment isn't the but factor that contributes to lower default run a risk.

Interest rate

Involvement rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk past property financing, and he or she may charge a higher interest rate to offset this hazard.

It'south not uncommon to see involvement rates from 4% to 10%. They could exist higher, as well. Nonetheless, each state has usury laws, which are regulations governing the maximum interest rate that can be charged on a loan. In addition to the varying interest rate, at that place are several repayment terms available:

- Fixed-charge per unit loan: The interest charge per unit and payment stay the aforementioned throughout the entire term. The principal balance of the loan is gradually paid down with regular payments.

- Adjustable-rate mortgage (ARM): The interest rate adjusts periodically.

- Interest-only loan: The buyer merely pays interest for a fix period, and so usually makes a large balloon payment toward the master.

Fixed-rate interest loans are most common because of the ease in tape keeping. Adjustable-rate mortgages fluctuate over fourth dimension and, if non actively monitored, tin can lead to changes in the principal and interest being miscalculated or missed altogether. Interest-only loans are most usually used with investors, especially for fix-and-flip loans.

Balloon payment

A airship payment is a former lump sum payment at the stop of a loan.

Loans with airship payments usually require monthly payments for a short period before the payment of the residuum of the principal balance at the end of the loan. This payment tin can be made from savings, past selling the property, or refinancing.

Balloon payments are fairly mutual with seller-financed notes because lenders seldom want to wait 20 or 30 years to go their money back. These payments can also increment the return for the investor, then savvy real manor investors may elect this as a term.

How to construction a seller-financing deal

Various possessor-financing structures can affect the heir-apparent's security in the property and the process for regaining title if the buyer defaults.

Promissory note and mortgage or deed of trust

A promissory note and mortgage (or deed of trust, depending on the state) is the virtually mutual form of owner financing. This is the same construction a bank would employ and is what people think of when they call back mortgage.

The note outlines the corporeality the heir-apparent borrowed and terms for repayment to the seller. The mortgage is a carve up certificate that securitizes the seller with the property in the issue of default. The buyer is put on the title with a deed and the mortgage is typically recorded in public records. A promissory note isn't recorded and the original should be held by the seller.

A note and mortgage is the almost secure form of financing for the heir-apparent and the seller.

Contract for human action

A contract for deed tin can also be called an agreement for deed or state contract installment, depending on the state of issuance. It's structured like a note and mortgage, only instead of the buyer receiving a deed and being placed on championship, the seller remains on championship until the debt is repaid in total.

Some sellers may cull this structure considering it'due south less time-consuming and more cost-constructive to regain marketable title of the property if the borrower stops paying. Many states permit eviction or forfeiture, which are faster and cheaper than a full foreclosure. The procedures for this vary from country to state and contracts for human activity aren't recognized in some states.

A contract for deed is a less secure form of financing for both the buyer and seller. Since the seller remains on the title while the buyer lives in and is responsible for the property, any liens or violations that become attached to the property during that period could negatively affect the seller.

Charter choice

A lease option is a form of owner financing where the buyer agrees to lease the home with the pick to buy it at the end of the agreement term.

The heir-apparent and seller agree on the buy price of the dwelling house earlier the lease starts and the seller typically receives a down payment. At the end of the charter term, the buyer tin can purchase the home or forfeit their charter option. If the buyer buys the home, payments fabricated during the lease period tin can be used toward the purchase price.

Owner financing lien position

All loans are categorized by position, such equally a first lien, 2d lien, so on. The lien position distinguishes the priority a loan has in relation to other debts or encumbrances on the property. The start lien is the about secure position.

Seller financing tin be used equally a second-position note to help a buyer purchase the property when they may non have the full amount to buy the home. For example, let'southward say a buyer finds a habitation for sale at $400,000 and has 20% ($lxxx,000) to put down. She qualified for a $300,000 banking concern loan, and then the seller decides to conduct financing for the remaining $xx,000, payable over 5 years. This owner-financed mortgage is secondary to the first mortgage from the bank, but is fully enforceable, like any regular mortgage. Hither's what those payments would look similar.

The first mortgage, payable to the bank:

| Loan amount | $300,000 |

|---|---|

| Interest rate | 4.5% |

| Number of payments | 360 |

| Monthly payment | $ane,520.06 |

Data source: Author calculations.

The second mortgage, payable to the seller:

| Loan amount | $20,000 |

|---|---|

| Involvement rate | half-dozen% |

| Number of payments (term) | 60 |

| Monthly payment | $386.66 |

Data source: Author calculations.

Owner financing documents and the Dodd-Frank Act

The documents used in owner financing vary depending on the type of construction used, but in most cases, there are two carve up documents:

- The note, which outlines how much is to be repaid and the terms of the repayment.

- The security instrument, which could be the land contract, mortgage, or act of trust.

The Dodd-Frank Human action made several changes to the mortgage industry, including possessor-financed residential loans. While much of the pecker focuses on debt collection and servicing rights, there were likewise revisions to who can originate seller-financed loans.

Before 2014, the person belongings the financing could create the note and mortgage themselves or have an attorney or a title company practice it for them. But the Dodd-Frank Human activity requires a licensed mortgage loan originator (LMLO) to underwrite and create any loans in which the buyer intends to reside in the belongings. You tin can hire a third-party LMLO to handle all of the required loan underwriting, including:

- pulling credit,

- determining the debt-to-income ratio,

- verifying identity and income, and

- creating and executing all paperwork.

If y'all intend to write or create the loan yourself, you demand a license unless yous qualify for i of the two exceptions:

- You ain the property you're holding financing for and simply create a loan for one property (that you didn't construct or act equally the contractor for) in a 12-month menstruation.

- You're a trust, manor, or entity holding financing for three or fewer properties that y'all own in a 12-month period and didn't construct or deed every bit the contractor for.

There are guidelines on specific terms such equally balloon payments, interest rates, and vetting processes. For this reason, even if you're not required to be a licensed mortgage loan originator, you should piece of work with a knowledgeable professional person who tin help you with the paperwork and underwriting.

It'south important to note that the Dodd-Frank Act doesn't use to:

- properties intended for investment purposes, such as rentals;

- vacant land;

- commercial properties; or

- non-consumer buyers, such as limited liability companies (LLCs), corporations, trusts, or express partnerships (LPs).

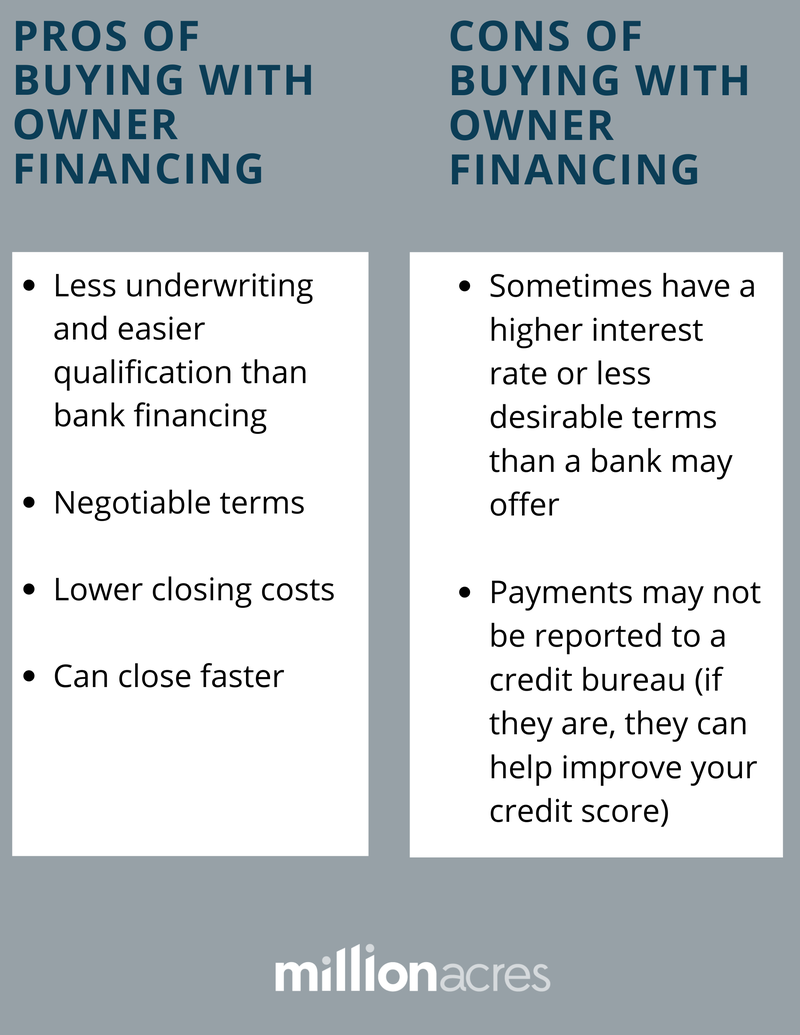

Why buy with owner financing? What are the benefits of owner financing?

Owner financing tin be beneficial for a heir-apparent or a seller. A seller may offer owner financing to reduce capital gains taxes from selling the belongings. A seller-financed loan breaks upwardly the gains over a catamenia of time.

Some investors offer financing on backdrop when they're prepare to retire to reduce taxes and create balance income. If the heir-apparent performs on the loan as agreed, the seller has created a passive income stream for many years.

Owner financing may as well be a good option if the seller has trouble selling the holding because information technology doesn't qualify for financing from a bank. Using owner financing gives prospective buyers the opportunity to purchase a property they may not have had access to without it.

Seller financing is an appealing choice for buyers considering information technology lets them purchase a property without having to borrow coin from a bank. There's typically less paperwork, fewer fees, and fewer qualifications to meet to be canonical. Not all buyers who request or use possessor financing to buy a habitation are unqualified. It may be that they don't qualify for a bank loan considering they're self-employed or lending has tightened in the current market place.

Click to overstate

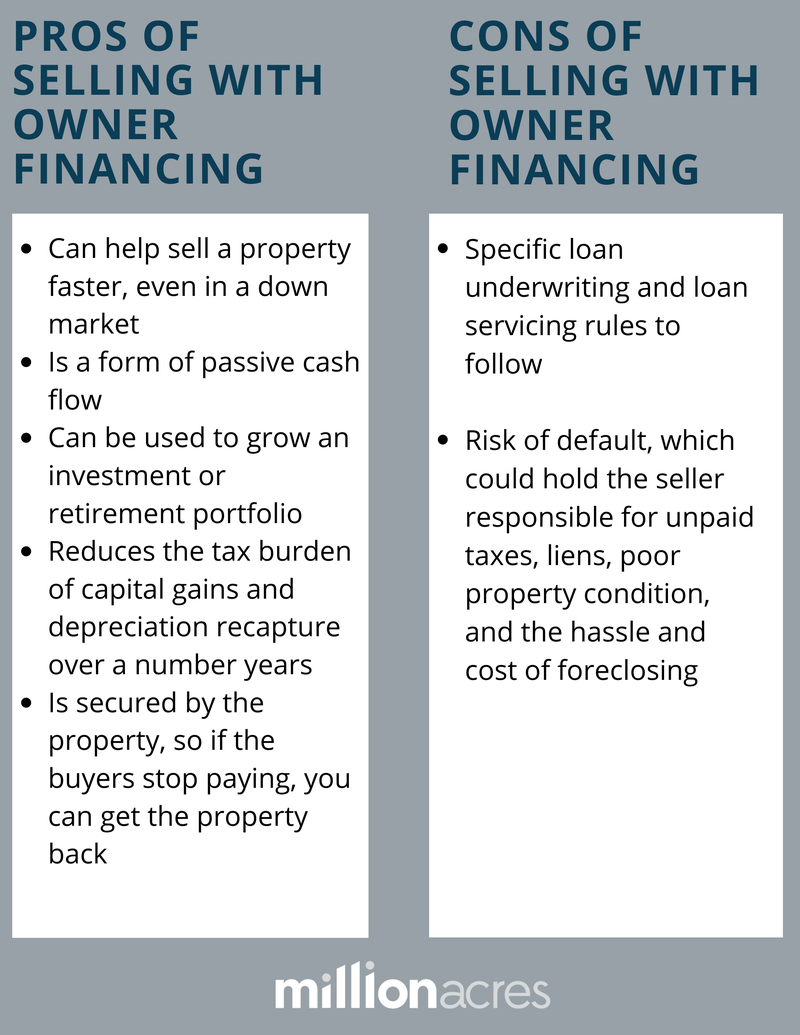

Why sell a property with owner financing?

Dorsum in the '80s, when interest rates were in the high teens and depression 20s, selling properties was difficult. Sellers were desperate to notice buyers, so many offered owner financing with lower interest rates than banks were offer.

Luckily, interest rates have get far more favorable in the past decade, then sellers may not demand to use possessor financing, merely certain tax advantages may incentivize sellers to offering it.

When a property is sold, it may be discipline to capital letter gains taxes in improver to depreciation recapture. Past creating a seller-financed loan, the tax hit from capital gains is cleaved up over the life of the loan rather than having it in ane tax year. It can also be a grade of passive income for the seller, who can use the monthly principal-and-interest payment to first living expenses in their retirement or grow their investment portfolio.

Click to enlarge

Important things to know near seller financing

Near possessor-financed loans are created by holding owners or investors for the tax advantages and greenbacks menses these loans generate. While these owners may exist experienced investors, they may not know the current laws regarding loan documentation, underwriting guidelines, record keeping, or contacting a borrower.

I've seen owner-financed loans in which the seller had cracking records with proof of payments for every payment fabricated past the heir-apparent, and I've seen seller-financed loans in which the possessor had no idea where the original loan documents were, what the rest of the loan was, or where tangible records of the payments were.

While seller-financed loans aren't regulated equally heavily every bit banks or servicing companies, in that location are specific requirements. For this reason, anyone who owns or creates a loan should educate themselves on the proper procedures or utilize a licensed servicing company.

A servicing company can handle several important tasks:

- Payment collection, including recording payments with the remainder due, paid-through date, and other important loan data. Servicing companies will study payment history to the credit bureaus, which is often beneficial for the buyer.

- Buyer outreach, which may include payment reminders, monthly statements, or delinquency notices.

- Loss mitigation, or efforts to collect on the loan if the heir-apparent stops paying.

Servicing companies charge a nominal monthly fee depending on the condition of the loan, such as paying or not-paying. A servicing company volition keep y'all compliant with the current laws, which makes for a more passive, hands-off investment.

Owner financing risks

For sellers offering possessor financing, the most substantial risk is the buyer not repaying the loan as agreed. You tin can have measures to reduce the likelihood of default, simply there's no way to guarantee a buyer can or will continue to pay.

Some ways to subtract this risk are:

- running a credit written report,

- verifying income,

- looking upwards by payment history,

- seeing the buyer's outstanding debts, and

- calculating a debt-to-income ratio.

The seller has the right to regain championship through legal activity, such as foreclosure or forfeiture, merely this takes time and can be costly. Sympathize your country's laws and procedures for regaining title if the heir-apparent defaults. Some sellers set the down payment aside in a split up account to cover any expenses in example the buyers stop paying.

For buyers inbound into a seller-financing understanding, the most substantial risk is how payments are tracked. If the seller services the loan themselves, their recordkeeping may not accurately reverberate the residue owed or the last payment made. Buyers should keep their own records of each payment made over the life of the loan so the remaining balance due can be verified.

Owner financing offers major advantages to both buyers and sellers. Just earlier you enter an owner-financed agreement, weigh the risks and consult a real estate attorney to ensure you lot understand the consequences, terms, and responsibilities of the understanding. This method of financing is definitely non right for everyone, simply it tin can be a useful tool when buying or selling real estate.

Got $1,000? The ten Top Investments Nosotros'd Make Right Now

Our team of analysts agrees. These 10 existent manor plays are the best ways to invest in existent manor correct at present. By signing up to be a member of Real Estate Winners, yous'll go access to our ten best ideas and new investment ideas every month. Observe out how you can get started with Real Estate Winners by clicking here.

Source: https://www.millionacres.com/real-estate-financing/articles/guide-owner-financing/

0 Response to "Best Way to Owner Finance a House in Nc"

Post a Comment